Buying a home requires a mortgage. The major banks in Canada, namely the Royal Bank, the Bank of Montreal, the Canadian Imperial Bank of Commerce (CIBC), the TD Bank, and the National Bank, influence Canadian mortgage rates. As of late April 2026, the interest rate for a 5-year fixed mortgage for major Canadian banks averages between 4.19% and 4.94%. Although minor lending institutions usually offer cheaper, limited-time deals, CIBC and RBC are offering the best fixed mortgage renewal options among the Big 5 banks, according to Ratehub.ca and WOWA.ca.

What is a mortgage?

A mortgage is essentially a loan taken out in order to buy a home, a piece of land, or some other form of real estate. When you decide to purchase your property with a mortgage, you agree with the lender, usually a bank, on repaying the mortgage principal (amount you borrow) and a share of the interest over a specific period of time. The property acts as collateral on the mortgage loan in case the borrower cannot fulfill the terms and conditions of the contract and fails to pay his loan. Most mortgages also usually have a fixed interest rate, and the monthly payment for it remains the same for the term duration. Each monthly payment contains a principal share (the initial loan amount) and an interest share (a percentage rate you are charged by your lender).

What Are Mortgage Rates?

A mortgage rate is an interest rate that lenders charge their clients for the loans (mortgages) granted. This rate can depend on various factors, such as the type of mortgage you acquire (variable-rate or fixed-rate), the term (loan repayment) period, your personal credit score, and the size of your down payment. Also note that most banks base the rate they charge on the prime rate.

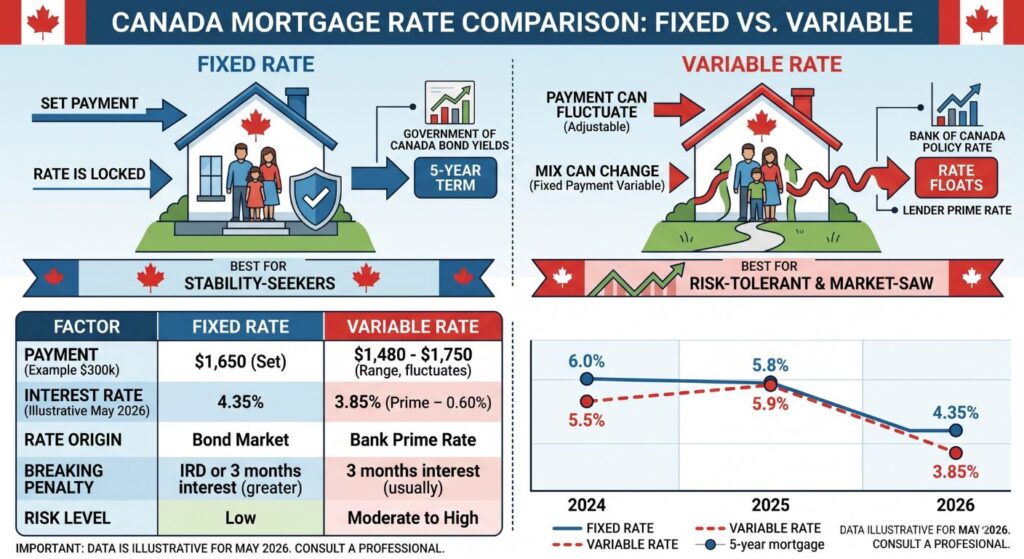

Fixed vs. Variable Rate

The two types of mortgage rates available in Canada are fixed and variable. Each has different pros and cons depending on your risk preference:

Fixed-Rate Mortgage

The interest rate applied to the mortgage does not change for the entire loan repayment period.

Benefit: The interest payment for each monthly payment remains the same throughout the term. This means you get payment certainty and budget planning. Fixed mortgages usually come with terms between 6 months and 10 years (though 1-, 2-, 3-, 5-, 7-, and 10 year mortgages are common).

Variable Rate Mortgage

Interest rates will change as they are tied to the Bank of Canada’s prime rate.

Benefit: While the monthly payment itself does not change with a variable-rate mortgage, the interest rate portion of it changes depending on movements in the prime rate. With adjustable-rate mortgages (ARMs), on the other hand, have your monthly payment directly affected by changes in the prime rate. If rates decrease, you save money; if they increase, your mortgage payments go up. Variables/ARMs are also flexible in nature but may offer payment uncertainty in the long run.

Open vs Closed Mortgage Term

Closed mortgages will charge you a fee for any mortgage overpayments. Open mortgages have greater flexibility for paying down your mortgage lump sum or paying it down sooner via larger mortgage payments.

What Is a 5-Year Fixed Mortgage?

A 5-year fixed mortgage is a mortgage that is locked in at a specific interest rate for the period of 5 years. Monthly payments are also fixed for this 5-year term. By locking in, the rate is guaranteed not to change within these 5 years. Once the 5-year fixed mortgage term is complete, you will have to re-mortgage, and your rate will depend on the market rates available at the time you choose to do so. According to the FCAC (Financial Consumer Agency of Canada), the interest rate is fixed for your specified term length and thus provides payment certainty for that term, while the renewal rate is market dependent at the time of maturity.

5-Year Fixed Mortgage Rates in Canada

5-year fixed mortgage rates offer a specific interest rate, along with your monthly payments guaranteed for 5 years. Due to its appeal as a stable, long-term mortgage solution, the 5-year fixed mortgage is currently the most popular type of mortgage term in Canada. The fixed nature of your mortgage rate will secure your borrowing and monthly payments for 5 years. This is the main advantage of the 5-year fixed term, offering budgetary certainty for a longer period of time than most alternative, more short-term options. Penalties for breaking this 5-year term can be very steep, however.

Why 5-Year Fixed Mortgage Rates Change

Your mortgage rate for a 5-year fixed mortgage term is guaranteed, so your monthly payments won’t increase/decrease for 5 years. However, the new rates themselves fluctuate every day based on many things, including interest rate decisions from central banks, anticipated future interest rates, and how the market performs.

Mortgage rates generally follow the general economic landscape; that’s why banks adjust rates in reaction to decisions and economic data.

5-Year Fixed Mortgage Best For?

A 5-year fixed mortgage would suit individuals and families who:

- Seek stability and payment predictability.

- Are risk-averse and want to shield themselves from interest rate hikes.

- Have plans to live in their home for the next several years.

Borrowers who anticipate substantial financial changes may look to variable-rate options and shorter mortgage terms.

Pros and Cons of a 5-Year Fixed Mortgage

Pros

- Long-term payment stability.

- Protection from fluctuating interest rates.

- Easier budgeting.

- Most widely available mortgage term.

Cons

- Less flexibility compared to short-term or variable mortgages.

- High penalty fees for early mortgage termination.

- Risk of missing out on lower rates should interest rates decline during the term.

Key Considerations Before Choosing a 5-Year Fixed Mortgage

Before committing to this 5-year fixed mortgage term, you need to take into consideration the following:

- How long you plan to be on the property is important.

- The penalties associated with early mortgage termination.

- How penalties are calculated by lenders and their specific terms and conditions.

- Your risk tolerance.

- It is often in your best interest to investigate your renewal options and calculate the penalties of early cancellation ahead of time, as the savings can often be significant.

Top 5 Banks for Fixed Mortgage Renewal (5-Year Fixed)

Rates shown are typically for insured or special offer categories as of April 2026:

CIBC

Offering a competitive 4.19% for 5-year fixed terms, currently the lowest among the top banks.

Why We Picked It

When comparing mortgage rates, it’s so important to know the rate you’re actually paying, and CIBC has both a wide selection of fixed-rate mortgages and transparent rates that we love. CIBC also has an extensive branch network if you prefer working with a mortgage specialist in person.

Why We Like It

CIBC has an excellent selection of mortgage products and publishes its posted rate, special offer, and APR rate (including fees) for each, giving you a complete picture of your options.

Why We Don’t Like It

You can start your application online, but then you’ll need to work with a CIBC mortgage specialist. If you prefer a digital-only option, CIBC (like any major bank) may not be the right fit.

Who It’s Best For

Homeowners who are thinking of switching to a Big Six Bank and are interested in exploring a variety of term options, or newcomers to Canada.

Pros and Cons of CIBC Bank

Pros

- Wide variety of mortgage terms, including short-term closed and open mortgages

- Special offers on the most popular 3-year and 5-year terms

- Extensive branch network for in-person application

- Offers three special mortgage programs for newcomers, including a foreign worker program

- Up to $4,500 cash-back offer when you switch your mortgage to CIBC and up to $3,500 on a new home purchase (Offers expire September 2, 2025)

- Offers CIBC Home Power Plan HELOC option

- Optional mortgage disability or life insurance

- Prepayment option of up to 10%, 15% or 20% depending on the product

Cons

- No online application options

- Posted rates are comparable to other major lenders

- Need a good credit score to qualify (unless you fall under the newcomer to Canada criteria)

- No three-year high-ratio mortgage option

Rates starting at approximately 4.29% for high-ratio mortgages.

Why We Picked It

RBC, another stalwart in the mortgage lending industry, offers the terms and rates you’d expect from Canada’s biggest bank, including the only 25-year fixed-rate mortgage in Canada. Its rates, however, aren’t as competitive as those of the other majors.

Why We Like It

As Canada’s biggest Schedule I bank, RBC offers a robust selection of fixed-rate mortgages, including the only 25-year fixed-rate mortgage in Canada. While its posted rates are in line with the other Big Banks, RBC offers a sound selection of discounted fixed rates.

Why We Don’t Like It

Like all of Canada’s Big Six Banks, even RBC’s special rates are higher than the best rates offered by other lenders via mortgage brokers.

Who It’s Best For

Homebuyers with good credit who want to work with Canada’s largest bank

Pros and Cons of RBC Royal Bank

Pros

- Wide selection of mortgage terms, including short-term and open mortgages, as well as Canada’s only 25-year fixed-term mortgage

- Discounted rates on popular terms, including both conventional and high-ratio mortgages for the 5-year fixed term

- Offers a full suite of complementary banking services, including the RBC Homeline Plan (mortgage plus credit line)

- 120-day rate hold

Cons

- High rates compared to other lenders

- You need a good credit score to qualify

- The 10% prepayment privilege is low compared to other lenders

- No three-year insured mortgage option

National Bank

Currently advertising a special 5-year fixed rate of 4.54%.

Why We Picked It

The smallest of Canada’s Big Six Banks, National Bank of Canada, has a healthy offering of fixed-rate options. While its posted rates are typical of the percentages you see from a major lender, it offers discounted rates that can save you thousands of dollars on your mortgage. Its business focus is in Quebec and Ontario, which may be a consideration if you’re outside of central Canada.

Why We Like It

The National Bank of Canada offers fixed-rate mortgages from three months to 10 years at similar rates to the other Schedule I banks, but with a healthy offering of discounted rates on terms between one year and seven years. There’s also a mortgage for the self-employed, which can be a great choice for workers or business owners who can’t provide standard proof of income.

Why We Don’t Like It

Like the other Big Banks on this list, the posted rates are high compared to what you can find with a mortgage broker. NBC also has most of its mortgage business in Quebec and Ontario, which may limit who can access its best offers.

Who It’s Best For

Homebuyers in Ontario or Quebec, especially self-employed workers or business owners.

Pros and Cons of National Bank

Pros

- Wide selection of mortgage terms, including short-term and open mortgages

- Discounted rates on terms between one and seven years

- Generous cash back offers for buying a home, switching your mortgage, or refinancing.

- Offers the All-In-One home equity line of credit product

- Mortgage solution for the self-employed with a 10% down payment

Cons

- The majority of mortgages are in Quebec and Ontario

- 90-day rate hold is shorter than other lenders’.

- No online application option

- No 3-year insured mortgage option

Special offers are hovering around 4.59%.

Why Choose TD Bank for Your Mortgage?

- Competitive Fixed and Variable Rates

- Access market-leading rates that fit your financial goals.

- Flexible Payment Options

- Choose from weekly, bi-weekly, or monthly payment plans to match your budget.

- Generous Prepayment Privileges

- Pay up to 15% of the original principal annually or increase your regular payments by up to 15%.

- Portability Options

- Transfer your mortgage to a new property without penalties.

- Specialized Mortgage Programs

- Explore cashback mortgages, insured high-ratio mortgages, and more.

Who Qualifies for TD Bank Mortgage Rates?

To qualify for TD Bank’s best mortgage rates, you’ll need:

- Good Credit Score

- A score of 680 or higher is typically required for the most competitive rates.

- Stable Income

- Provide proof of steady income, such as pay stubs, T4 slips, or tax returns.

- Sufficient Down Payment

- A minimum of 5% for insured mortgages or 20% for uninsured mortgages.

- Acceptable Debt-to-Income Ratio

- Your total monthly debts should not exceed 42% of your gross income.

Who It’s Best For

This can give peace of mind to homebuyers since the interest rate on their mortgage will not rise if interest rates do; however, they will not benefit if interest rates go down.

Pros & Cons of TD Bank

Pros

- Their interest rates are mid-range, so they are not as high as other options

- Their payment vacations and pauses come in handy when life throws a wrench into your finances

- They are rated #1 for online banking apps

- Immediate response for online mortgage pre-approval

Cons

- There are lower interest rates available at other lenders offering similar features

- As a big-six bank, they have stricter lending criteria to qualify

BMO (Bank of Montreal)

Offering 5-year fixed rates starting at 4.64%

What We Like It For

Not only does BMO offer one of the largest selections of fixed-rate terms at competitive rates, but they also offer the longest rate hold of any major bank (130-days). You also can enjoy full banking services and products from BMO including a home equity line of credit.

Why We Like BMO

Being Canada’s oldest bank means they have a very well-rounded mortgage selection from very short to long terms, open to convertible, so you will surely have the options you are looking for. They also offer a Smart Fixed mortgage, on which you can get a lower interest rate if you are willing to accept more restrictive prepayment options, which can be a better option if you know for sure you will not be breaking your mortgage during the term. While their posted rates are similar to the Big Six Banks in the country, the discounted mortgage rates are still quite competitive.

Why We Don’t Like BMO

Compared to digital-only mortgage lenders with advanced online application tools, you need to speak with a BMO mortgage specialist by phone or in-person.

Best For

Home buyers who value the complete service that a major bank offers and want a secure fixed-rate mortgage for the entire term of the mortgage.

BMO (Bank of Montreal) Pros and Cons

Pros

- Offers a wide selection of fixed-rate terms (short- and long-term), including convertible, open, special rates for key term lengths

- Choice of regular fixed-rate or Smart Fixed Mortgage (lower rates but stricter prepayment conditions)

- Offers a 130-day mortgage rate hold (reportedly the longest among major banks)

- Allows for 20% prepayments (10% on Smart Fixed)

- Access to Homeowner Readiline (combined mortgage with a line of credit)

- Consultation available by phone or in-person with a mortgage specialist

Cons

- Does not have online mortgage application feature

- Requires a good credit score to qualify

What are the requirements for getting the lowest mortgage rates?

Over the past 10 years, Canadian interest rates have shifted from historic lows to 30-year highs. This has fundamentally impacted how buyers can qualify for a mortgage and the stress tests they are subject to, as a measure of risk. However, even with the higher qualifying thresholds, here are the top 5 criteria to get the lowest mortgage rates in Canada:

Good credit score

You will typically require a FICO score of 680 or higher. If applying with others, they will need a good credit score as well. Exceptions are made but increase depending on how many you require.

Clean credit report

You should ideally have no more than one missed payment in three years and none that have been sent to collections.

Proof of income

Typically require pay stubs or income tax documents; a two-year history is usually required for bonus or commission-based income.

Reasonable debt-to-income ratios

A loan to income ratio of above 44% will make it difficult to qualify for the best rates. Additionally, a housing-to-income ratio (mortgage payment, heat, property taxes, and 50% of condo fees) must not exceed 39% of your gross monthly income. A credit score of 680 or higher is needed for a 39% housing-to-income ratio or 35% for anything lower than that.

Remember this when considering qualifying for the lowest mortgage rate, as all applicants must pass the government’s stress test. Stress testing is a procedure used by lenders where your debt-to-income ratios are recalculated using a rate higher than the actual rate on the mortgage. If you qualify at the time for a 3.25% mortgage, they may recalculate it as though you will actually pay 5.25% to ensure you can still manage payments if the rate were to rise.

Stable employment

If you are new to your job, some lenders will only offer the best rates to individuals who have been working in the same role or company for a minimum of one year. While some lenders don’t have this condition, the more requirements you have, the more difficult it will be to obtain a favorable rate.

Choosing the correct fixed-rate mortgage term

Your decision on how long your term should be largely comes down to what you believe interest rates will do. You should opt for short-term fixed-rate mortgages if you think rates will fall. You will be able to renew your mortgage more frequently and re-evaluate the rate if circumstances permit and/or the rate is favorable. If you anticipate rates to increase, you should go with long-term fixed-rate mortgages, as they protect you from rising rates.

Conclusion

Canada’s best mortgage rates for 2026 differ depending on who you’re comparing with, what you’re comparing it to, and, of course, who is looking to buy. Looking at our comparison, the insured vs. Uninsured status will be what determines the highest fixed rate compared to the lowest variable rate depending on lender pricing, bond yields, etc., and actual rates will also be dictated by how well your credit, your income, and your ability to save impact how a lender underwrites the mortgage for you.